Overall analysis

For several months now, governments and the European community have been warning us of the need to continue with cooling and containment measures to combat the inflation which, since the end of the pandemic, has hit the economies of all countries hard. Governments have gradually scaled back stimulus measures and the European Central Bank has implemented its policies of gradually raising interest rates. The result is becoming visible in a sector as sensitive as construction, where new building permits continue to fall, in turn reducing the volume of materials used.

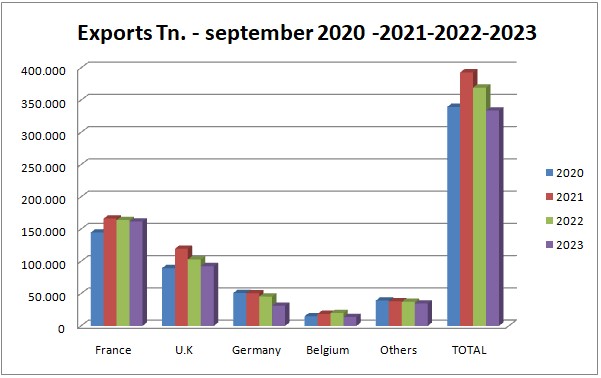

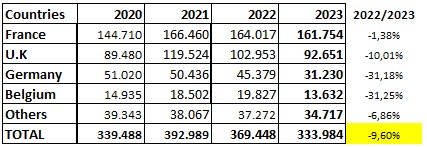

Analysis by country:

France

In terms of slate imports, France is the country with the best data, losing only -1.38% of its volume compared with 2022 (from 164,017 to 161,754 tonnes). The use of slate in this country is most concentrated in renovation, a sector that continues to show great strength with major implementation commitments for 2024 and a large stock of old houses reaching the end of their useful life and in need of replacement. The competitiveness of slate in France, despite price rises in recent years due to rising costs, remains a key factor.

United Kingdom

The slate sector recorded a decline of 10.01%, representing a gradual cooling of the property market, which has boomed in recent years. The slate sector needs to put this year’s negative figures into perspective because, while recognising the size of the fall, they mean that we are roughly back to 2020 values, which are the averages that this market would normally show in favourable circumstances.

Belgium

Belgium saw a fall of 31.25% (from 19,827 to 13,632). As in the case of the United Kingdom, we need to put the data into perspective and conclude that this is a return to normal levels, once the post-pandemic effects on the property market as a safe haven have passed.

Other countries

In line with our analysis, the volume accumulated in other countries at the end of September was 34,717 tonnes, representing a decrease of -6.85% compared with 37,272 tonnes in 2022. These are countries where slate is not a traditional material and where there is not a large network of slate installation specialists to guarantee market growth, although significant growth has been observed in recent years in countries such as the United States and Ireland, with accumulated imports at the end of September of 8,160 tonnes and 7,403 tonnes respectively, and Denmark with 2011 tonnes.

Conclusion

The slate sector is watching developments closely, as it is to be hoped that once the economy has cooled and interest rates have returned to more acceptable levels, the downward trend in the property sector can be halted immediately, particularly where new construction is concerned. The latest inflation figures seem to confirm this, with inflation rates less galloping and more stable than in recent months. In Spain, the social measures that the new government is beginning to unveil are awaited with concern, particularly the reduction in the 40-hour working week, which could have a significant impact on our competitiveness, given our heavy dependence on production labour.

Source:Clúster da Pizarra de Galicia.