The situation in the slate market continues along the same lines as in recent months; demand remains very high and puts pressure on production, which is pushed to its maximum, without being able to fully satisfy its customers.

1 – General analysis.

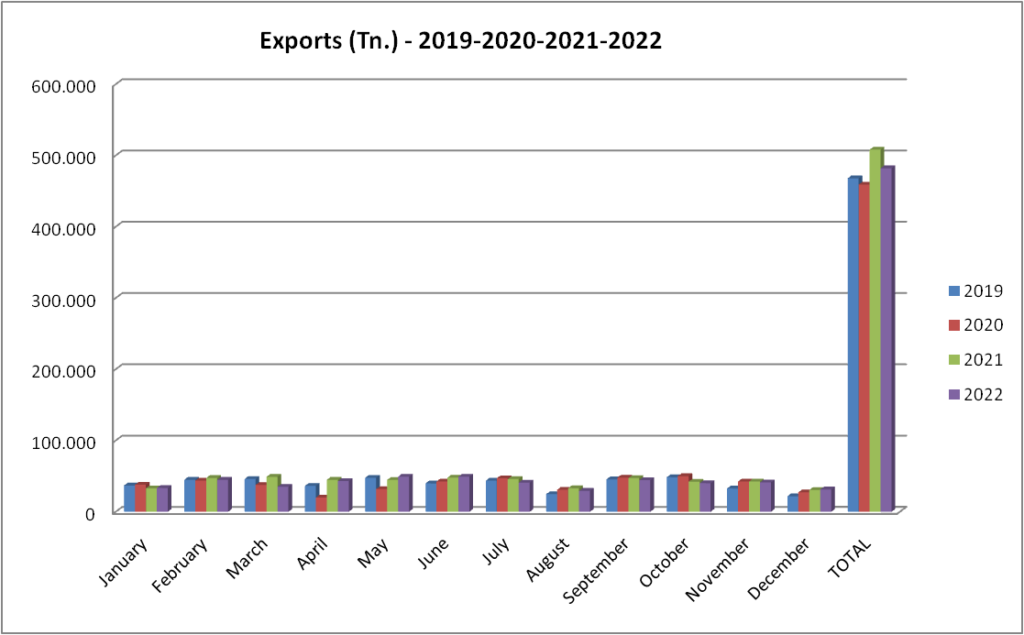

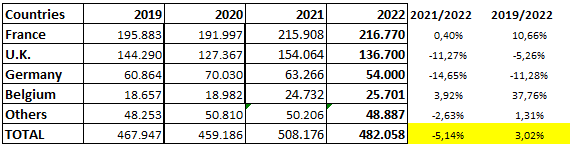

This shows how the volume of exports in tonnes at the end of November is -5.14% compared to the same period in 2021, all this without available stocks and with delivery times that have not been reduced.

The average value of the price per tonne has increased by 20.80% due to the increase in tariffs and probably the impact of sales of premium quality ranges. However, this inflationary dynamic did not translate into an improvement in production margins, due to the constant increase in the prices of the main supplies: fuel, energy and explosives. At the end of the year, the situation worsened with the abolition of the 20 cent subsidy on fuel and the sharp rise in social security contributions.

Indications, that the inputs are down, are not helping either. If we compare the data for 2022 with previous years, we can see that exports in tonnes have not increased despite the strong demand and that it is quite similar to the years when, in addition to supplying the markets, the quarries were able to manufacture to maintain their stocks to an appreciable extent.

We can see another significant example of this weakness. If we compare the data for 2022 and 2021 (two years with the same situation of high demand and minimal stocks), export volumes fall from 482,058 Tn. in 2022 to 508,176 Tn. in 2021, i.e. a loss of almost 26,118 Tn. exported (-5.1%).

2 – Study by country.

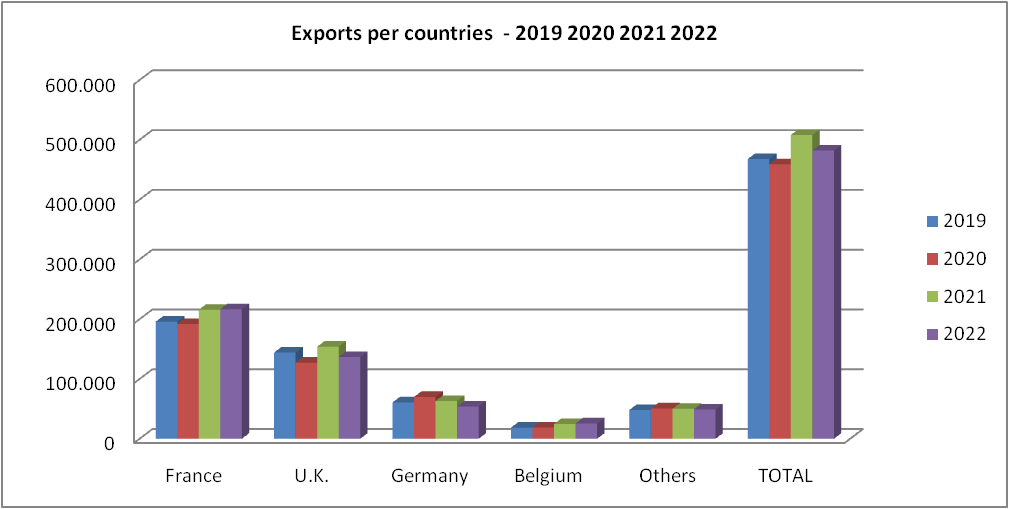

FRANCE

It continues on the regular line of last year, repeating practically the same volumes (216,700 Tn.). Although potential demand in France is currently much higher, there is great tension in the market with supply problems and very long delivery times. Slate has gained market share this year due to the impact of gas and electricity costs on our competitors’ materials and increased investment in home improvements.

UNITED KINGDOM

It shows a loss of -11.27% compared to 2021 with 17,364 Tn. less. The causes may be multiple in a context where distributors are still looking for production in Spain:

- The effects of the Brexit slowdown on transport and customs;

- the problem of the lack of capacity of quarries to meet demand, concentrated in a few quarries traditionally oriented towards the English market;

- the model used in these markets, which is larger, more difficult to produce and consumes more slate, may have shifted the production of some companies to less complicated markets for these operations;

GERMANY

It also shows negative signs (-14.65%) compared to 2021. The situation is comparable to the UK: weak quarry production and complicated manufacturing patterns, with very specific designs that make it difficult for workshops to be agile.

For years, there has been a gradual loss of volumes in favour of the United Kingdom, which has long been the second largest importer of slate.

BELGIUM

Although export figures are more modest than those of previous countries, due to its size, the Belgian market continues to show strong growth (+37.76% compared to 2021). It is still a market based on high-end qualities, with high purchasing power and, with support for construction reforms, continues to bear fruit.

Conclusion:

We are still living in uncertain times, the energy crisis continues to hit the markets, generating inflation, reducing production and creating instability in the form of shortages and unbalanced delivery times for materials.

The overall figures remain at last year’s level, with a slight drop, no stock available in the sector and strong demand pressure, further compounded by the alternative material production problems of our competitors who suffer more from their dependence on gas and electricity.

The slate sector is working at the limit of its capacity, the lack of investment in recent years in the mining industry due to the financial crisis in Spain, the lack of manpower despite the automation of the workshops, the new safety requirements and the regulatory restrictions for the opening of new quarries do not help to solve this problem.

Source: Clúster da Pizarra de Galicia – February 2023.